We’re familiar with the idea that the economy can and should affect elections. The connection is borne out empirically (Roosevelt’s victory in 1932 following the depression, his landslide reelection in 1936 amid economic growth, Johnson and Reagan winning huge reelections during the boom periods of 1964 and 1984, Carter losing in the 1980 recession and Bush Sr. losing in the 1992 mini-recession) and theoretically, either from the principle of retrospective voting (giving a political party credit or blame for its stewardship of the economy) or prospective voting (giving the keys of the economy to the party that you think can do the job). A good starting point here is Steven Rosenstone’s book from 1983, Forecasting Presidential Elections.

Indeed, the principle of economic voting (“It’s the economy, stupid”) has become so familiar that it was overgeneralized to apply to off-year (non-presidential) elections as well. The evidence appears to show, however, that off-year elections are decided more by party balancing; see previous discussions from 2018 and 2022:

What is “party balancing” and how does it explain midterm elections?

The Economic Pit and the Political Pendulum: Predicting Midterm Elections

But this year a presidential election is coming, and the big question is why Biden is not leading in the polls given the strong economy. There are lots of reason to dislike Biden—or any other political candidate—so in that sense the real point is not his unpopularity but the implications for the election forecast. As the above-cited Rosenstone and others have pointed out, pre-election polls can be highly variable and so in that sense there’s no reason to take polls from May so seriously. In recent campaigns, however, with the rise of political polarization, campaign polls have been much more stable.

As we discussed the other day, one piece of the puzzle is that perceptions of the economy are being driven by political polarization. This is not new; for example:

A survey was conducted in 1988, at the end of Ronald Reagan’s second term, asking various questions about the government and economic conditions, including, “Would you say that compared to 1980, inflation has gotten better, stayed about the same, or gotten worse?” Amazingly, over half of the self-identified strong Democrats in the survey said that inflation had gotten worse and only 8% thought it had gotten much better, even though the actual inflation rate dropped from 13% to 4% during Reagan’s eight years in office. Political scientist Larry Bartels studied this and other examples of bias in retrospective evaluations.

That said, it does seem that polarization has made these assessments even more difficult, even when people are characterizing their own personal financial situations.

Here’s the question

The above is all background. Here’s my question: how is the effect of the economy on political attitudes and behavior supposed to work? That is, what are the mechanisms? I can see two possibilities:

– Direct observation. You lose your job or find a new job, or you know people who lose their jobs or find new jobs, or you observe prices going up or down, or you get a raise, or you don’t get a raise, etc.

– The news media. You read in the news or see on TV that unemployment or inflation has gone up or down, or that the economy is growing, etc.

Both mechanisms are reasonable, both in the descriptive sense that people get information from these different sources and also in the normative sense that it seems fair, to some extent, to use economic performance to judge the party in power. Not completely fair (business cycles happen!) and sometimes they lead to bad incentives such as pro-cyclical expansionary policies, but, still, there’s a strong logic there.

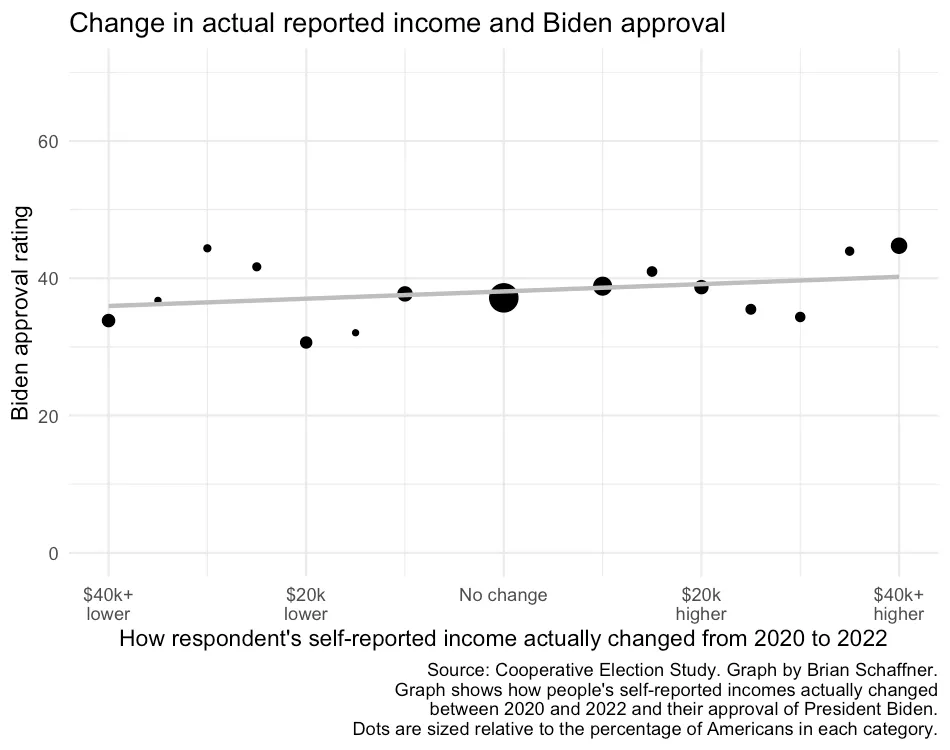

The thing I’m struggling with is how the direct observation is going to work. A 2% change in economic growth, or a 4% change in the unemployment or inflation rate, is a big difference, but how will it be perceived by an individual voter. Everybody’s experience is different, and it’s not clear that any simple aggregation will apply. If you think of each voter as having an impression of the economy, which can then affect that person’s vote, then, fine, the average impression will correspondingly affect the average vote—but any bias in the impressions will lead to a bias in the average, and there’s no reason to think that people’s perceptions are unbiased or even close to that, even in the absence of political polarization.

As I wrote a couple days ago:

Wolfers’s column is all about how individuals can feel one way even as averages are going in a different direction, and that’s interesting. I will say that the even the comments that are negative about the economy are much less negative than you’d see in a recession. In a recession, you see comments about people losing everything; here, the comments are more along the lines of, “It’s supposed to be an economic boom, but we’re still just getting by.” But, sure, if there’s an average growth of 2%, say, then (a) 2% isn’t that much, especially if you have a child or you just bought a new house or car, and (b) not everybody’s gonna be at that +2%: this is the average and roughly half the people doing worse than that. The point is that most people are under economic constraints, and there are all sorts of things that will make people feel these constraints—including things like spending more money, which from an economic consumption standpoint is a plus, but also means you have less cash on hand.

So, lots of paradoxes here at the intersection of politics, economics, and psychology: some of the components of economic growth can make people feel strapped—if they’re focusing on resource constraints rather than consumption. . . .

People have this idea that a positive economy would imply that their economic constraints will go away—but even if there really is a 2% growth, that’s still only 2%, and you can easily see that 2% disappear cos you spent it on something. From the economist’s perspective, if you just spent $2000 on something nice, that’s an economic plus for you, but from the consumer’s point of view, spending that $2000 took away their financial cushion. The whole thing is confusing, and I think it reflects some interaction between averages, variations, and people’s imagination of what economic growth is supposed to imply for them.

My point is not that people “should” be feeling one way or another, just that the link between economic conditions and economic perception at the individual level is not at all as direct as one might imagine based on general discussions of the effects of the economy and politics.

This makes me think that the view of the economy from the news media is important, as the media report hard numbers which can be compared from election to election. For example, back in the 1930s, the press leaned Republican, and they gave the news whatever spin they could, but they reported the economic news as it was; similarly for the Democratic-leaning news media in 1980 and 1984.

My current take on the economy-affecting-elections thing is that, in earlier decades, economic statistics reported in the news media served as a baseline or calibration point which individual voters could then adjust based on their personal experiences. Without the calibration, the connection between the economy and political behavior is unmoored.

The other issue—and this came up in our recent comment thread too—is what’s the appropriate time scale for evaluating economic performance? Research by Rosenstone and others supports a time horizon of approximately one year—that is, voters are responding to the relative state of the economy at election time, compared to a year earlier. So then the election turns on how things go in the next few months. Normatively, though, it does not seem like a good idea to base your vote on just one year of economic performance. So then maybe the disconnect between the economy and vote preference is a good thing?

Indeed, it is usually considered to be politically beneficial for a presidential term to start with a recession and then bounce back (as with Reagan or, to a lesser extent, Obama) than for a term to start good but end with a downturn (as with Carter)—even though up-then-down corresponds to higher economic output than down-then-up. Again, any individual voter is only experiencing part of the story, which returns us to the puzzle of why we should expect economic experiences to aggregate in a reasonable way when transformed to public opinion.

Summary

Journalists and political scientists (including me!) have a way of talking about the aggregate effect of the economy on voting, with the key predictors being measures of economic performance in the year leading up to an election. There’s a logic to such arguments, and they fit reasonably well to past electoral data, but the closer you look at this reasoning, the more confusing it becomes: Why should voters care so much about recent performance? and How exactly do economic conditions map onto perceptions? What are the roles of voters’ individual experiences, their observations of local conditions, and what they learn from the news media? There’s a lot of incoherence here, not just among voters but in the connections between our macro theories and our implicit models of individual learning and decision making.

P.S. Some discussion here from Paul Campos. I remain bothered by the gap in our political science models regarding how voters aggregate their economic experiences. At some level, yeah, sure, I get it: a good economy or a bad economy will on the margin make a difference. The part that’s harder for me to get is how this is supposed to work when comparing one election to another, years later.